‘Sense-maker’ in chief: Expect the unexpected (and do it proactively vs. reactively) is the post-Covid-19, new mantra for ESG Leaders.

Leaders believe that every company and industry has a unique materiality signature that evolves over time. Proactive management of material issues enabled 1) competitive advantage, 2) an opportunity to understand and shape the issues; and 3) a window to reduce the value at stake from the material issue.

However, ESG leaders find justifying a rigorous process and focus to be difficult for 3 main reasons:

And once a process is settled on, three further factors complicate the materiality assessment itself:

Help is now at hand!

These insights come from a global listening tour over 25 countries, 75 companies and 98 ESG leaders, sustainability professionals, chief risk officers, chief sustainability officers and strategy heads.

Download the New ESG Playbook here.

Forget CSR. ESG leaders agree unanimously that unlike ‘CSR’ predecessors (historically more likely to be ‘bolted on vs. baked in’ initiatives), ESG is driving a fundamental change to the business at every level. The tipping point has been the pace, volume, complexity and magnitude of external change in investment resources, policy and consumer and employee preference.

However, the sheer volume of expert, media, academic and business coverage on ESG can be daunting to non-initiates.

Feel the force. ESG leaders find explaining ESG internally as a set of positive forces (vs. mere risk mitigation) is beneficial. Forces include:

It’s a competition for ‘white space’. Sustainability may be the biggest story telling opportunity for the next decade. Yet with everyone now pushing an ESG narrative, it is a competitive play (for investment, employees, NGO leniency, policy neutrality, media share, consumer preference, etc.) and finding narrative ‘white space’ is difficult.

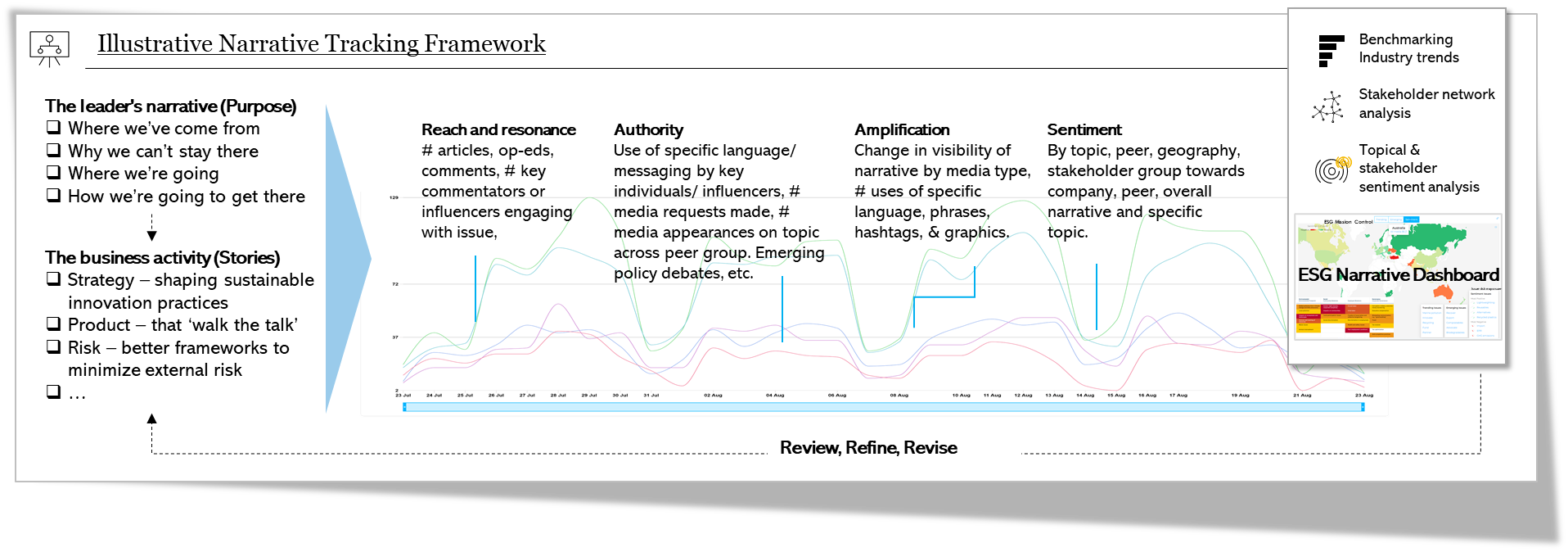

And Data led. Weaving together an inspiring, clear and coherent ‘value creation and loss prevention’ company-wide narrative is considered far from a solved problem. ESG leaders stress the need for a scientific and data driven approach to dynamically shape the ESG narrative.

This needs to support:

‘Sense-maker’ in chief: Expect the unexpected (and do it proactively vs. reactively) is the post-Covid-19, new mantra for ESG Leaders.

Leaders believe that every company and industry has a unique materiality signature that evolves over time. Proactive management of material issues enabled 1) competitive advantage, 2) an opportunity to understand and shape the issues; and 3) a window to reduce the value at stake from the material issue.

However, ESG leaders find justifying a rigorous process and focus to be difficult for 3 main reasons:

And once a process is settled on, three further factors complicate the materiality assessment itself:

Help is now at hand!

These insights come from a global listening tour over 25 countries, 75 companies and 98 ESG leaders, sustainability professionals, chief risk officers, chief sustainability officers and strategy heads.

Download the New ESG Playbook here.

Forget CSR. ESG leaders agree unanimously that unlike ‘CSR’ predecessors (historically more likely to be ‘bolted on vs. baked in’ initiatives), ESG is driving a fundamental change to the business at every level. The tipping point has been the pace, volume, complexity and magnitude of external change in investment resources, policy and consumer and employee preference.

However, the sheer volume of expert, media, academic and business coverage on ESG can be daunting to non-initiates.

Feel the force. ESG leaders find explaining ESG internally as a set of positive forces (vs. mere risk mitigation) is beneficial. Forces include:

It’s a competition for ‘white space’. Sustainability may be the biggest story telling opportunity for the next decade. Yet with everyone now pushing an ESG narrative, it is a competitive play (for investment, employees, NGO leniency, policy neutrality, media share, consumer preference, etc.) and finding narrative ‘white space’ is difficult.

And Data led. Weaving together an inspiring, clear and coherent ‘value creation and loss prevention’ company-wide narrative is considered far from a solved problem. ESG leaders stress the need for a scientific and data driven approach to dynamically shape the ESG narrative.

This needs to support: